Maintaining market share in commercial banking is about more than products, rates, or pricing strategies. Today’s commercial clients expect seamless, valuable, and easy-to-navigate experiences. Yet despite ongoing investments in technology, service delivery, and relationship management, many institutions continue to face familiar challenges:

- Retaining clients and reducing attrition

- Improving onboarding and implementation experiences

- Accelerating lending and credit decision processes

- Increasing relationship growth and share of wallet

- Reducing operational friction and improving service responsiveness

At Verde Group, we frequently work with organizations that are investing heavily in customer experience improvements yet still struggle to achieve the outcomes they expect. In many cases, customer feedback is collected, analyzed, and discussed, yet organizations continue to face challenges with customer retention, growth, and loyalty.

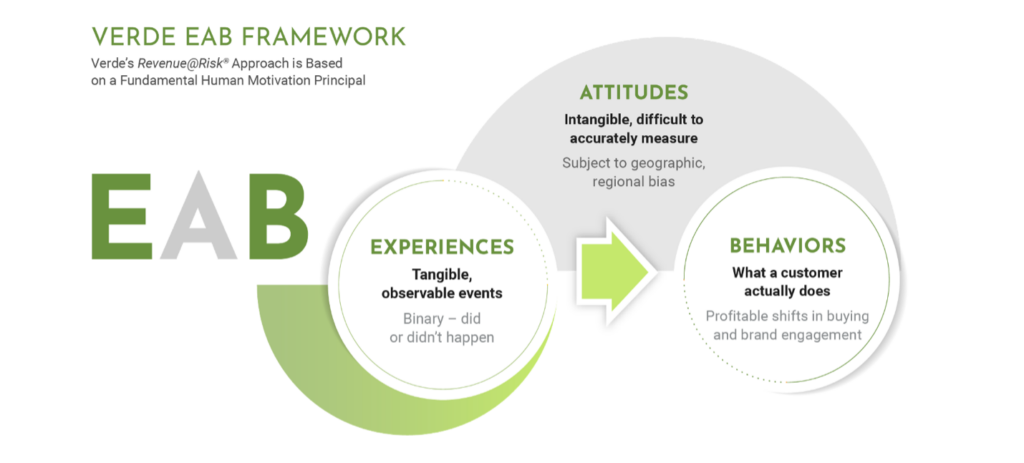

The real question isn’t whether organizations are listening to their customers. It’s which experiences most strongly drive customer loyalty, deepen relationships, and create long-term value.

The Cost of Friction

These challenges are not unique to commercial banking. Across industries, organizations are discovering that customer loyalty is shaped less by the products they offer and more by the quality of the experiences they create.

Customer experience research conducted in the insurance sector identified responsiveness, status updates, time-to-resolution, expectation setting, process clarity, empathy, and communication as among the most influential drivers of customer satisfaction. In fact, knowledgeable service (87.8%), care and empathy (87.3%), ease of process (83.9%), and timely updates (81.7%) emerged as some of the strongest contributors to positive customer experiences.

The findings reinforce a simple but important lesson: customers place significant value on clear communication, responsive service, and confidence in the people serving them. While products and pricing remain important, the experiences surrounding those offerings often determine how customers evaluate a relationship.

Even more telling was where organizations chose to focus their improvement efforts. Many of the highest-priority initiatives focused on operational enhancements, such as digital service capabilities, flexible communication options, proactive outreach, performance monitoring, and workflow optimization, rather than changes to the core product offering.

The implication is clear: reducing friction and making it easier for customers to do business often has a greater impact on loyalty than introducing new products or features.

Not All Customer Problems Carry the Same Risk

Most organizations collect customer feedback. The challenge is determining which issues have the greatest impact on customer behavior and business performance.

Commercial banking institutions receive feedback across dozens of touchpoints from onboarding and treasury management services to lending processes, relationship management, and digital banking experiences. The temptation is to treat every issue equally. In reality, some friction points have a far greater influence on customer loyalty, retention, and relationship growth than others.

This is one of the most common challenges Verde Group encounters when helping organizations evaluate customer experience performance. Businesses often have no shortage of customer data. What they need is a better understanding of which experiences have the greatest impact on customer behavior and business outcomes.

Organizations that see the greatest return from their voice-of-customer programs are not necessarily the ones collecting the most feedback. They are the ones who identify, prioritize, and address the experiences most likely to influence customer decisions and the long-term value of the relationship.

The real question isn’t simply what matters to customers. It’s what matters most.

Looking Beyond Products to Experience

To better understand what drives customer loyalty, organizations must look beyond products and services and examine the broader customer experience.

Commercial clients rarely evaluate their banking relationship based on a single interaction. Instead, their perception of value is shaped over time through a series of experiences from onboarding and implementation to service requests, digital interactions, relationship reviews, and ongoing support.

When those experiences are seamless, customers are more likely to deepen their relationships with a financial institution and expand their banking relationship. When they are complicated, inconsistent, or difficult to navigate, trust begins to erode.

Many of the challenges organizations face are not rooted in the products themselves. They stem from unclear processes, inconsistent communication, delays in resolving issues, a lack of proactive engagement, and uncertainty about where to turn for support. While these issues may seem operational, they often significantly affect how customers perceive value and whether they choose to continue or expand a relationship.

The encouraging news is that many of these challenges lend themselves to relatively straightforward improvements. Clear ownership, proactive communication, regular relationship reviews, accessible self-service resources, and ongoing education can all help strengthen customer relationships and improve overall satisfaction.

The underlying principle is simple: customers are more likely to remain loyal when organizations make it easy to do business, proactively support their success, and consistently demonstrate value throughout the relationship lifecycle.

Where the Biggest Opportunities Exist

Verde Group research has identified two primary areas where commercial banking institutions can make the greatest impact: simplifying administrative complexity and closing the knowledge gap in customer support. Focusing on these opportunities helps reduce friction, increase satisfaction, and drive long-term growth.

Simplifying Administrative Complexity

One of the most significant opportunities identified through the research was reducing administrative complexity.

Many customers feel that routine banking processes are more complicated and time-consuming than they need to be. Whether opening accounts, managing documentation, navigating onboarding requirements, or obtaining status updates, unnecessary effort can create frustration and slow the growth of the relationship.

In an environment where businesses are continually seeking efficiencies, friction becomes more than an inconvenience; it becomes a business problem.

Organizations across industries are responding by investing in omni-channel service models, digital self-service capabilities, flexible communication options, and workflow improvements that increase transparency and accessibility. Customer experience research consistently identifies responsiveness, process clarity, expectation setting, and communication as critical drivers of satisfaction and loyalty.

The objective is not simply to digitize existing processes. It is to create experiences that provide reassurance, visibility, trust, and convenience.

As one participant noted, “If it ain’t broke, don’t fix it.”

That mindset continues to influence customer behavior across industries. Adoption is most successful when digital tools are intuitive, convenient, and require minimal effort to learn. When customers see clear value and little disruption, they are far more willing to embrace new ways of interacting with an organization.

The takeaway is straightforward: reducing friction supports stronger customer relationships, increased satisfaction, and long-term growth.

Closing the Knowledge Gap in Customer Support

Another major opportunity centers on knowledge and confidence within customer-facing teams.

Commercial clients expect clear, informed guidance when they reach out with questions, concerns, or requests. Whether discussing lending options, treasury solutions, cash management services, or digital banking tools, customers expect frontline employees to provide accurate information and actionable advice.

When representatives cannot confidently answer questions or explain available solutions, resolution times increase, confidence declines, and trust in the relationship weakens.

Across industries, customer expectations are shifting toward seamless omnichannel service. Customers increasingly want the flexibility to engage through digital, self-service, and traditional channels depending on the complexity of their needs.

Meeting these expectations requires more than technology. It requires knowledgeable employees who can provide consistent information regardless of the channel through which a customer engages.

Organizations that invest in frontline enablement, training, and knowledge-sharing create more confident employees, more productive conversations, and stronger customer relationships.

The Bigger Picture: Experience Drives Growth

These findings point to a broader shift occurring across industries.

At Verde Group, our work consistently demonstrates that customer experience can no longer be viewed as a “nice-to-have” initiative. It directly influences growth, adoption, retention, loyalty, and revenue performance.

Many organizations continue to face challenges such as:

- Customers disengaging because processes feel overly complex

- Trust eroding when communication lacks transparency

- High-potential products underperforming because the surrounding experience falls short

- Resources being spread too thin across low-impact improvement initiatives

The organizations that perform best are those that focus their efforts on the experiences most closely tied to:

- Customer retention and loyalty

- Relationship growth and share of wallet

- Product adoption and usage

- Long-term customer value

The business implications are substantial. A landmark Harvard Business Review study by Bain’s Frederick Reichheld and W. Earl Sasser Jr. found that cutting customer defection rates by just 5% increased profits by 85% in one bank’s branch network — a pattern echoed across other service industries.

The Path Forward

The lesson is simple: value is not created through a single product, transaction, or interaction. It is built across every touchpoint in the customer journey.

As commercial customers continue to evolve, the institutions that serve them will need to do the same. The organizations that succeed will be those that move beyond assumptions and develop a deeper understanding of how customer experience connects to business performance.

This is where Verde Group helps clients move beyond traditional satisfaction measures and focus on the experiences that most strongly impact customer loyalty, retention, and growth.

Because in commercial banking, value is not simply delivered. It’s experienced.